The Organisation for Economic Cooperation and Development (OECD) is the latest body to wade into the inheritance tax debate – on a global scale.

Source: OECD May 2021

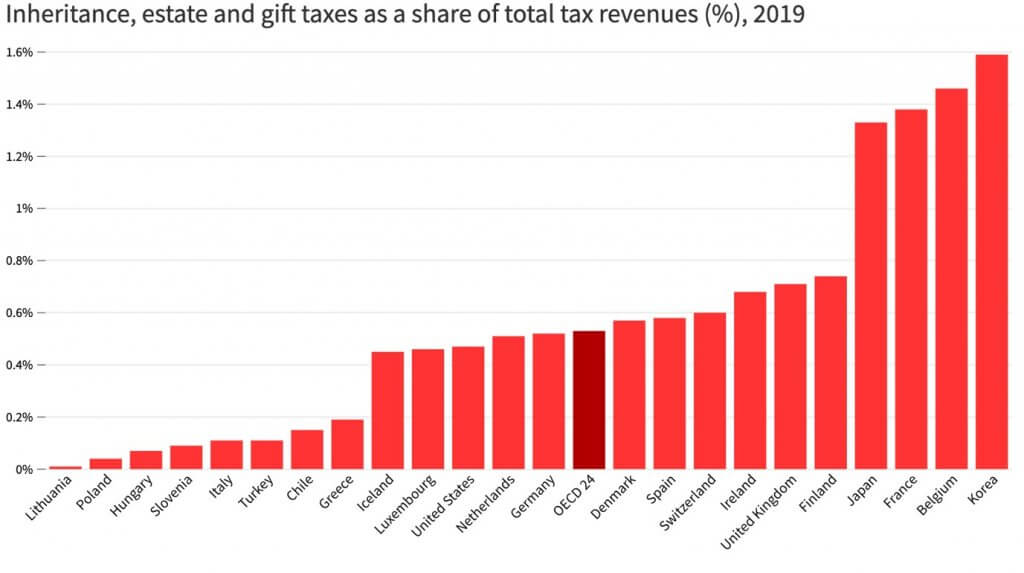

Inheritance tax (IHT) and similar gift/estate taxes raise a very small portion of overall tax revenues in the OECD countries that have them, as the graph above shows. Even in the UK, which levies that tax at above the OECD average, IHT produces less than £1 in every £100 of tax revenue. The OECD thinks this is a missed opportunity.

In a report published in May 2021, the OECD says, “Inheritance taxation can be an important instrument to address inequality, particularly in the current context of persistently high wealth inequality and new pressures on public finances linked to the Covid-19 pandemic”. The report makes a range of recommendations on how to structure inheritance taxation, including:

- It is preferable to levy tax on the recipients rather than on the donor’s estate – the opposite of the UK approach. However, the OECD did not support the idea that transfers should be taxed as income, a suggestion that has emerged from some think tanks in this country.

- Ideally, a tax based on beneficiaries should cover gifts and bequests they receive over their life, subject to a modest lifetime exemption. The OECD is no fan of regular or renewable exemptions – a feature of UK IHT – because of the scope they offer for avoidance. It accepts that the lifetime approach creates increased administrative and compliance costs.

- Exemptions or reliefs for business assets should be carefully designed and alternatives considered. The OECD questions the UK design, highlighting that “relief for business and agricultural assets predominantly benefit the wealthiest households, significantly reducing the effective tax burden on some of the largest estates”.

- Legislation should not allow planning through trusts to significantly reduce the tax burden on wealth transfers.

- There should be a consistent tax treatment of unrealised capital gains between gifted and bequeathed assets. Here the OECD echoes comments from the UK’s Office for Tax Simplification (OTS) own reports on capital taxes.

Will the Chancellor pay any heed to the OECD’s proposals? We await his response to the OTS reports on the future structures of inheritance tax and capital gains tax which could appear in the autumn Budget. In the meantime, if estate taxes concern you, it could be worth putting plans in place now, while the current rules exist.

The value of tax reliefs depends on your individual circumstances. Tax laws can change. The Financial Conduct Authority does not regulate tax advice.

Content correct at the time of writing and is intended for general information only and should not be construed as advice.