With allowances frozen or cut, you may have underpaid tax for 2023/24.

Your tax position may have changed for the last year without you really noticing. Consider the following:

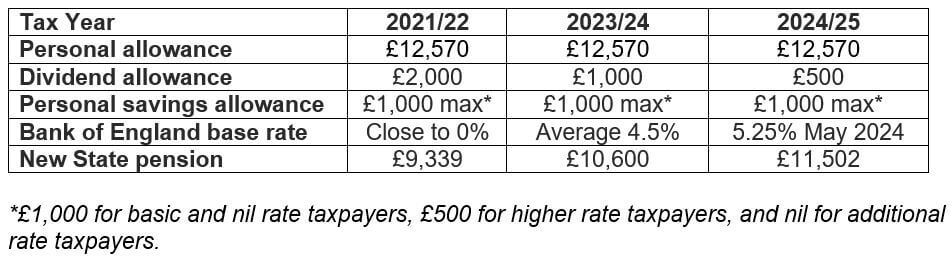

Rising income – for example in the form of pensions, dividends or interest – and frozen or reduced allowances are a recipe for creating more taxpayers and higher tax bills. This is becoming increasingly clear as some people are discovering that they became taxpayers in 2023/24 despite their only income being a State pension (new or old, supplemented by the additional State pension). For those affected, HMRC will issue a simple assessment tax bill as the Department of Work & Pensions provides details of payments made.

If you do not already complete a self assessment tax return, it is your duty to inform HMRC of your income if a new tax liability arises because:

- Your interest has exceeded your personal savings allowance, and/or:

- Dividends breached the dividend allowance.

You can inform HMRC of a change of circumstances through your online personal tax account, if you have one, or by trying to call them (good luck with that!). In most circumstances, you will not have to complete a full self assessment return: you can check whether you have to file at the government website. If you do not tell HMRC about your interest receipts, be aware that building societies and banks (including those located offshore) automatically report information to HMRC.

A similar situation applies to greater payments for capital gains tax where the annual exempt amount has fallen from £12,300 in 2021/12 to £6,000 in 2023/24, and just £3,000 in the current tax year.

Careful planning may help you to sidestep HMRC’s growing slice of your income and gains, but, as ever, expert advice is needed to avoid the traps.

Tax treatment varies according to individual circumstances and is subject to change.

The Financial Conduct Authority does not regulate tax advice.

Content correct at the time of writing.