A Taper Sulk not a Taper Tantrum

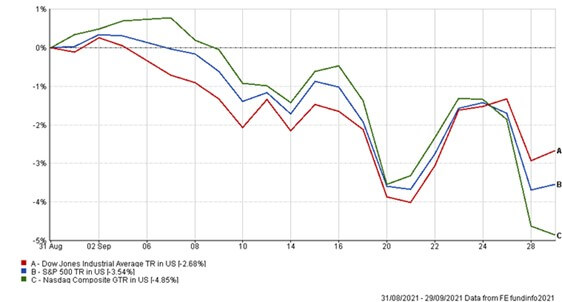

Apparently one of the historical realities of the US stockmarket is that typically it performs poorest during the month of September… certainly maintaining that undesirable record this year then. On average, September is the month when the US’s three leading indices – Dow Jones Industrial Average, S&P 500, Nasdaq – usually perform the poorest. An annual drop-off that is coined the ‘September Effect’.

The US Big Three – September performance (local currency)

Source: Financial Express Analytics

Inflation, asset tapering and interest rates

Of course, such is the importance and influence of the US stockmarkets, this weakness and volatility has rippled across global stockmarkets too. So what’s driving investor concerns this month. Well, it is basically three things:

- Is higher inflation proving more permanent than at first thought?

- When will Central Banks start withdrawing support by asset tapering?

- Is this the trigger for Central Banks to raise interest rates sooner than later?

The answer to the first question is still in the balance. Clearly disrupted supply chains, fuel crises and employee wage strength are inflation building, as shown in higher than expected inflation numbers – but are these factors still temporary and will they eventually wash through? The answer to the other two questions is that, bar any further systemic shock, these are going to happen. It’s just a matter of when.

The US Federal Reserve, The Bank of England, The European Central Bank are all trying to provide as much forward guidance to markets with regards monetary policy. Unfortunately, after some seismic monetary stimulus post-pandemic market sell-off, monetary policy is now going to tighten and the narrative about when that is going to happen is being brought forwards.

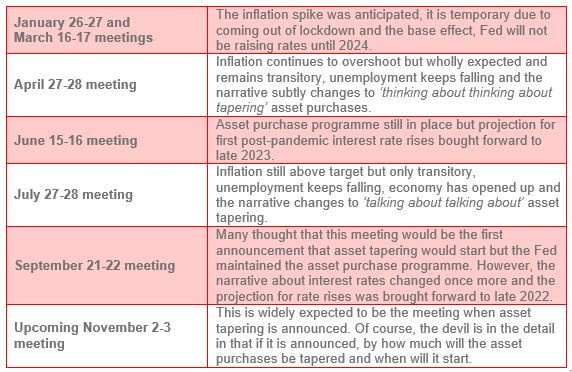

The Fed’s changing narrative

If we look at what the world’s most influential Central Bank has been telling us this year, you can see the narrative keeps changing at every meeting.

One can see the forward guidance the Fed keep giving the markets and that the day of monetary tightening by the Fed is coming ever closer. This is currently spooking markets once again, hence why we have seen government bond yields widen as their prices fall and equity markets start stuttering as investors look to reduce risk in the short-term.

A return to Q1 conditions?

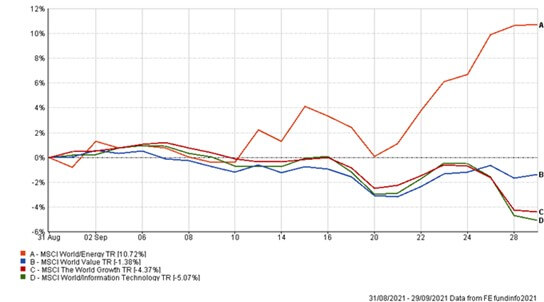

Not quite. Yes, inflationary pressures appear to be building again as mentioned and some cyclical sectors are outperforming lockdown winners again, as we can see from comparing the Global Energy sector against the Global Information Technology sector over September in the chart below. A comparison that we drew earlier in the year during the value, cyclical rally.

However, this does not necessarily mean that Value stocks are performing well overall. They currently are vs. Growth stocks as we can also see in the chart below, but only really in the last few days. And Value stocks have still lost money over the month too, just that in the very near-term they have held up better.

MSCI World Energy vs. MSCI World Information Technology and

MSCI World Value Index vs. MSCI World Growth Index – September (local currency)

Source: Financial Express Analytics

Don’t panic but keep listening

Markets are currently wrestling with Central Bank monetary policy, trying to second guess when and how they are going to tighten policy going forwards. The tapering of asset purchase programmes is arguably priced into markets now so investors are now worrying about interest rates – when will they be raised, by how much and how frequently.

Naturally, this is causing volatility within risk assets but it is the ‘risk-free’ assets – US Treasuries, UK Gilts, German Bunds etc. – that are suffering the most as they are highly interest rate sensitive.

However, even when interest rate rises are eventually announced – which we still don’t anticipate for some time I might add – cash deposit rates are still going to be very meagre indeed and nowhere near inflation levels. This means that investors must still invest in risk assets in order to achieve the potential for inflation beating returns. So even though September is shaping up to be a month to forget, we believe that this is not the start of a drawn-out bear market.

This article reflects the view of the Chase de Vere Portfolio Management Team.

It is not financial advice. If you require financial advice, please speak to your financial adviser.

Past performance is no indicator of future returns.

Content correct at the time of writing and is intended for general information only and should not be construed as advice.