Q2 2023 Update

Global economic growth surprised positively in the first quarter of 2023 following China’s reopening and an unusually warm winter lifted the European economy grappling with an Energy Crisis. Markets duly responded with strong returns in the first half of the quarter, however the collapse of Silicon Valley Bank (SVB) in March dragged markets lower for a period. SVB’s issues bear little resemblance to the bank failures during the Global Financial Crisis in 2008/09. The quick response from Central Banks to launch new liquidity programs restored investor confidence and the markets finished the quarter in a relatively buoyant mood.

Our macro views haven’t changed since the last review and many of our expectations are firmly playing out, particularly on the continued downtrend in global inflation and China’s reopening path. US inflation has fallen to 5% from a peak of 9.1%, EU inflation has declined to 6.9% from peak of 10.1% and UK has declined to 10.1% from peak of 11.1%, building the case for Central Banks to pivot to lower interest rates in the second half of this year. Chinese reopening has been swift and economic growth is improving sharply as the consumer draws-down savings and the dominant Chinese property sector jumps back to life after a near two year decline. We are therefore increasingly more confident for the full year and beyond.

However, it would be unwise to sound the all-clear on the global growth outlook in the short-term, given the rapid tightening in monetary policy combined with a further contraction in bank lending to the economy following the mini banking scare, and we remain cautious. Our core expectation remains firmly that we see Developed Market (DM) economies in aggregate falling into a mild recession in 2023 which the manufacturing survey data and key recession indicators suggest, however we believe some of this is broadly priced into markets. Relatively strong household and corporate finances are likely to limit the downturn to a mild recession, as well as improving global inflation trends, and strong Chinese growth will dovetail with weaker DM growth and support global growth in the latter part of the year.

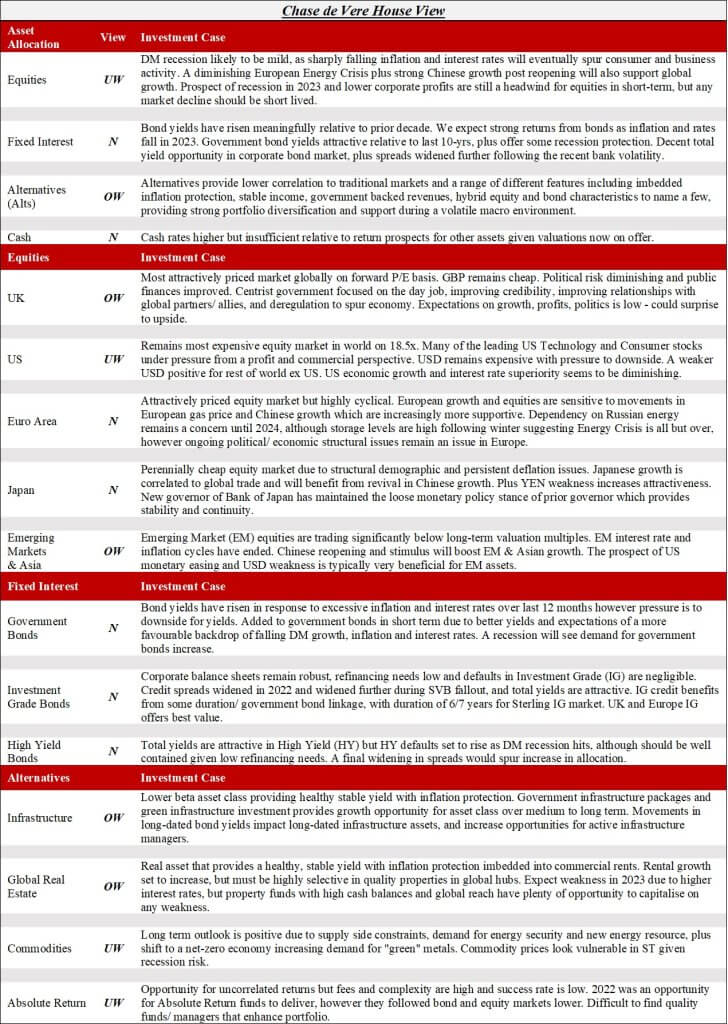

At this juncture, we have maintained a neutral (N) view on Fixed Interest, an overweight (OW) view to Alternatives and underweight (UW) view on Equities is also maintained. The portfolios still have ample risk and have performed well in up markets relative to peers and benchmarks since the low point in September last year. An opportune time to increase equities will materialise over the course of the year. We strongly believe, 2023 is the year many of the negative macro events of 2022 will reverse and we are seeing this play out, which will support markets over the course of 2023.

Economic Outlook 2023

We believe the global growth outlook will improve as we progress through 2023, and any recession will be mild and brief, due to:

- Inflation falling (disinflation). Historically major outbreaks of inflation subside relatively quickly 1-2 years after peak. The pandemic is the primary reason for the inflationary boom and as we move further and further away from the pandemic, we will likely witness an inflationary bust or a period of rapid dis-inflation. All major components of inflation including commodity prices, food prices, energy prices, transportation costs, supply chain costs have fallen rapidly from peak levels, and with sticky components of wages and housing costs set to finally ease, the outlook for inflation is very supportive and we expect a return to much lower inflation over next 12 months. Falling inflation incrementally boosts consumer and household purchasing power as more money is made available to spend elsewhere, supporting growth in the economy.

- Interest rates peak and decline in the second half of the year. Interest rate hiking cycles are coming to an end. The US Federal Reserve (The Fed) moved from near 0% to 5%, similarly the UK Bank of England (BoE) moved from near 0% to 4%. The global economy will continue to labour under the strain of higher interest rates and the interest rate sensitive sectors of housing and banking are vulnerable, hence the SVB collapse. The pressure for Central Banks to change policy direction is high, and with US inflation at 5% and interest rates at 5%, we are fast approaching normal levels of inflation but with excessively tight monetary policy. The US Federal Reserve is the lead Central Bank globally and they set the direction for interest rates globally. We expect one more hike from the Fed then a pause, which will set the scene for a move lower in interest rates globally, supporting economic growth 6 to 9 months later.

- Chinese reopening boosts global growth and lifts crucial property market. China’s reopening has been swift and the economy is registering strong growth in the first quarter of the year. The Chinese housing market has jumped to a 2-year high and is a major driver of consumer confidence as most wealth in China is tied up in property. Excess savings built up during lockdown are being drawn down rapidly with retail sales jumping 10.6% year-on-year in Q1. These improving growth dynamics in the second largest economy in the world supports global growth.

- European Energy Crisis is now on last legs. Gas storage facilities across Europe will end this winter 55% full, the highest level on record for Europe at the end of winter. The average levels from 2015 to 2021 were 33% and 2022 was a low of 26%. Europe has double the gas storage this year relative to last and will very likely be at maximum storage levels as they move into next winter. European natural gas prices have duly fallen by a stunning 87% since their peak in late August 2022. If the mild weather continues through summer and protracted heatwaves avoided, the European Energy Crisis is all but over, supporting European and UK growth. For example, annual energy bills for a typical household in the UK could drop to around £2,024 during the third quarter of this year, c.19% below the government’s Energy Price Guarantee.

- Global Financial Conditions improving. The “mini” banking crisis has consequently brought future interest rate expectations down as well as long-term bond yields, which has a resulting impact of lowering future borrowing costs. There has also been a pick-up in liquidity from the Fed to support the banks during the recent mini bank crisis. The US Dollar and commodities have also declined meaningfully from their peak levels in 2022. Therefore, the cost of “doing business” is now easier than it was 6-12 months ago, which typically positively impacts growth in 6-9 months’ time and will soften the depth of recession.

Markets well supported, despite prospect of a recession in the short-term

We expect the DM recession to be mild and relatively brief and markets have priced in much of the bad news, however, market volatility will remain elevated until the Central Banks finally change course on policy and cut rates, and the recession passes without issues.

We believe bonds are well supported in this environment with the prospect of lower inflation and interest rate cuts on the horizon, supporting fixed rate paying assets. Roughly 80% of the global bond market now offers yields over 4%. Non-US equity valuations including the UK, Europe, Emerging Markets and Japan are attractive and below their long term average valuation levels, and significantly below the valuation of the US equity market. The US equity market has hoovered up a lot of capital over the last decade but the tide is slowly turning and international investors as well as US domestic investors are starting to gradually favour non-US equity markets.

Long-term return prospects remain attractive as one would expect after a year of sharply negative returns for asset classes and a meaningful rise in the risk-free rate. A rising risk-free rate (cash rates), is typically challenging for risky assets, however the rise in the risk-free rate is now over, we believe. Investor sentiment indicators remain close to depressed levels, hedge funds are net-short and fund managers have raised cash levels suggesting much of the selling and repositioning has occurred and when investors finally turn bullish, the return from markets has historically been powerful.

We believe a cautious approach is still warranted at this stage given interest rates have still not officially been cut, and remain in restrictive territory, however, an opportunity to increases equities in the portfolios will materialise over the course of the year. We expect global growth to pick-up towards the back-end of this year on continued improvement in Chinese growth, easier global financial conditions, and DM Central Banks finally cutting interest rates, which will ease pressures in the banking system and will further support global growth in later part of this year and into next.

Probabilities, history and valuations remain on our side as we move through 2023. If we look at decades of market data, the probability of a better return year for markets is very high after such a terrible previous year. And 2022 was one of the worst years for bond and equity markets ever. If the recession is mild as we expect, any further market declines will be limited and short lived. We are confident the full year will be positive for portfolio returns.

Top-3 Risks To Outlook

- Interest Rate Risk/ Policy Error – the full economic impact of higher interest rates occurs with a variable lag, therefore economies are still absorbing interest rates that occurred many months ago. Interest rates increase borrowing costs and tighten financial conditions and, therefore, slows an economy down. That is their intention and there is a risk that Central Banks have gone too far. Higher interest rates also often unearth stress points in the economy, typically areas where excessive risk taking, such as the case with SVB, or excessive debt overload has occurred. Major systemic imbalances in the economy are low currently and the banking sector is closely regulated with any problems quickly resolved, but we remain on high alert for issues caused by higher interest rates.

- Recession Risk – the recession is now well anticipated which gives us confidence that it will be mild, however it still has to occur and pass without issue. As growth slows, it can unearth weak points. We believe recession is likely to occur if we look at indicators that have a high predictive power of forecasting recessions such as the US government bond yield curve, money supply growth and bank lending standards. All indicators suggest a recession is likely in the US as well as Europe over the next 12 months.

- Geopolitical Risk – any escalation of the Russia-Ukraine War is an obvious risk to stability and growth. However, the avenues for escalation from here are narrow. Recent engagements with China suggest China is looking to play peacemaker, which will crystallise a similar response from the US and Europe. We believe a ceasefire or settlement is much more likely than expected. The China-Taiwan risk will be an ever present risk for markets for many years to come, however should it occur it would be highly damaging to the Chinese economy and a risk to the authority of the Chinese Communist Party within China, and for that reason we believe the risk is low.

To discuss your investment strategy please contact your Chase de Vere financial adviser.

Important information

The value of your investment and any income from it can go down as well as up and you may not get back the full amount you invested.

Past performance is not a reliable indicator of future performance.

Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.

Information was obtained from proprietary and non-proprietary sources deemed reliable by Chase de Vere.

Where the qualified Investment Manager has expressed views and opinions, they are based on current market conditions and their professional judgement and are subject to change.

The information contained within this update is for guidance only and does not constitute advice which should be sought before taking any action or inaction.

Prices were correct at the time of writing.